Executive Summary: Asia credit outperformed its EM peers this week, trading firm despite a fragile US–Iran ceasefire backdrop, with IG spreads tightening 1–5bps. Ex-Asia EM credit had a volatile and net weaker week, as renewed US–Iran / Strait of Hormuz tensions kept oil prices elevated and risk premia higher. Approximately $2.4bn flowed into EM hard-currency funds. The EM Agg widened ~2.7bps WoW; CDX.EM43 fell ~26cts; HY underperformed IG across the board.

Market Visualizer

Regional Credit Developments

🇨🇳 Asia Credit: Investment Grade & High Yield

- Asia IG: Spreads tightened 1–5bps WoW. Benchmark China property names saw solid demand.

- GLPSP: Plunged 6–7pts with no clear catalyst ahead of FY25 results announcement.

- Ex-China HY: Closed +0.25–0.5pts on the week.

- Mineral Resources: Priced two-tranche USD 6yr / 8yr deal, upsized from $500m to $650m per tranche; both tranches traded ~1pt lower on the break.

- Genting: Priced USD 750m perpNC5.5 and USD 500m perpNC10y; both bonds traded down ~1pt on softer end-demand.

- Dalian Wanda: Priced $150m 3yr bond at 12.5%; traded 0.25pt lower on the bid side.

- Vanke: Secured bondholder approval for debt restructuring (40% upfront repayment, 60% one-year extension) — third onshore bond extension since December 2025. Bonds largely unchanged after falling 2–3pts the prior week.

🌏 Asia Credit: Frontier & Sovereign

- Philippines: Fitch revised outlook to Negative while affirming BBB rating, citing concerns over medium-term growth headwinds from Middle East energy shocks and slowing public sector investment.

- Thailand: Moody’s revised outlook to Stable from Negative; quasi-sovereign linked issues saw buying.

- Pakistan: Returned to USD bond market with $500m 3-year sovereign bond, upsized to $750m on demand. Central bank confirmed receipt of $1bn from Saudi Arabia’s finance ministry — final tranche of the $3bn deposit package.

- Frontier sovereigns: Underperformed on profit-taking flows as oil prices rose.

- Vedanta: On track for demerger into five separately publicly listed companies, effective May 1.

- Coronado Global Resources: Considering sale of its Curragh coking coal mine in Queensland, Australia.

- Japfa Pte (Ba3/B+): Conducting roadshow next week for USD 5NC2 new issue.

🌍 EM Ex-Asia Credit: CEEMEA

- Romania (ROMANI): +3/+5bps wider. PSD withdrew ministers on April 22–23, leaving the government a minority after PM Bolojan refused to resign over austerity disputes; PSD plans to file a no-confidence vote in the coming days.

- Ukraine (UKRAIN): -1.25/+0.25pts; B35/B36s underperformed. EU €90bn loan approved following Hungary’s Orban electoral loss; EU accession talks advancing.

- Lebanon (LEBAN): -2.25pts. Ceasefire extended three weeks but residual fragility weighed on bonds.

- Metinvest (METINV): +0.25/+0.50pts. Full redemption of April 23 bonds from internal cashflows; 2027/2029 bonds in focus.

🌍 EM Ex-Asia Credit: MENA & Africa

- MENA IG (KSA / ADGB): Traded defensively, finished modestly wider.

- Senegal: +2.3pts on positioning; AfDB disbursements remain frozen.

- Mozambique: +1.6pts.

- Angola: Heavy turnover with capped gains despite higher oil.

- Egypt: Underperformed (−1.75 to −3pts across the curve) on Middle East tensions.

🌎 EM Ex-Asia Credit: Latin America

- Colombia (COLOM 10Y): -0.75pts. Tender offer for 9 bonds ($12bn+ principal, 2035–2061); pre-priced by the market.

- Ecopetrol (ECOPET 10Y): -1.125pts. Moody’s downgrade to Ba2/Negative from Ba1/Stable, reflecting heightened government interference risk and reduced reliability of the Fuel Price Stabilization Fund (FEPC) mechanism. Separately, announced acquisition of a 26% stake in Brazil’s Brava Energia.

- Braskem (BRASKM): +0.50/+3.25pts; long-end lagged. Novonor agreed to sell 50.1% voting stake (34.3% total capital) to an IG4 Capital-backed fund. Petrobras waived its tag-along rights and signed a new shareholders’ agreement with the incoming fund.

- Raizen (RAIZBZ): +0.25/+0.50pts. Creditor negotiations ongoing; binding agreement still pending.

- Aeromexico (AEROMX 2031): -2.75pts. 1Q26 results: revenue +13% YoY; EBITDAR +5%; fuel cost headwinds.

- Aegea (AEGEBZ): -3.5/-1.5pts. Second S&P downgrade in three weeks (B+ to B with Negative outlook), reflecting weaker 2025 leverage metrics in delayed financial statements. Follows S&P’s April 1 cut (BB- to B+) and negative review actions from Moody’s and Fitch in early April.

- Ecuador (ECUA): -0.80/-0.20pts. Staff-level agreement at 5th IMF review; $400m disbursement unlocked.

Geopolitical & Macro Watch

- US–Iran: Ceasefire optimism from the prior week reversed; oil remains bid; Strait of Hormuz risk persists.

- China–US: Beijing is sending two giant pandas to the United States ahead of a planned Trump–Xi summit in mid-May.

- Israel–Lebanon: President Trump confirmed a three-week extension to the ceasefire (originally expiring April 26). LEBAN bonds closed -2.25pts.

Week Ahead

- Japfa Pte (Ba3/B+): Roadshow for USD 5NC2.

- Pakistan: Sovereign follow-through after upsized $750m deal.

- Vanke: Demerger mechanics post-bondholder approval.

- Vedanta: Demerger into five listed entities effective May 1.

- Raizen: Creditor negotiation update expected.

- GLPSP: FY25 results.

www.gembridgecapital.com

DISCLAIMER

This document is strictly confidential and is being provided to you for informational purposes only. It does not constitute an offer to sell or a solicitation of an offer to buy any securities or financial instruments. The information contained herein has been obtained from sources believed to be reliable but is not guaranteed as to accuracy or completeness. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice.

AI Generation Notice: Portions of this content may have been generated or assisted by Artificial Intelligence (AI) technologies. Users should independently verify critical data points. Past performance is not indicative of future results.

Executive Summary: Ex-Asia EM credit traded with elevated dispersion over the week, lagging a firmer macro backdrop. Risk-on conditions on 14 April gave way to mixed and choppy price action through 15–16 April. Flows remained skewed toward selling into strength across most regions, with selective positioning in CEEMEA, LatAm, and corporate names driven by country-specific and headline developments rather than broad spread compression.

Market Visualizer

Market Performance & Flows

📅 14 April — Risk-On Open

- HY Bonds: Rose approximately +25c to +1.5pts on the day.

- IG Spreads: Tightened by -1bp to -15bp.

- CDX.EM: Improved approximately +28c.

- Flow Drivers: Strong real money and CTA demand; supported by easing geopolitical tensions and improved macro sentiment.

📅 15 April — Softening Momentum

- HY Bonds: Ranged approximately -50c to +15c on the day.

- IG Spreads: Ranged -4bp to +4bp.

- CDX.EM: Near flat (~-5c from lows).

- Flow Drivers: Better selling dominated; dispersion increased on headline-driven moves.

📅 16 April — Underperformance vs. Macro

- HY Bonds: Moved between -75c and +1pt.

- IG Spreads: Ranged -4bp to +3bp.

- CDX.EM: Widened modestly (~-15c).

- Flow Drivers: Selling into strength remained the dominant pattern; ex-Asia EM credit underperformed broader macro conditions.

Regional Credit Developments

🌍 CEEMEA & MENA

- Lebanon: Bonds gained +20–30c on 16 April following reports of a 10-day ceasefire with Israel; hedge fund demand was observed despite ongoing real money selling. Earlier in the week, IMF headlines indicated potential fast-track financing of $800m–$1bn, generating two-way flows.

- Zambia: Remained in focus during IMF discussions in Washington; investor attention centred on debt restructuring mechanics, including DCC trigger risks and growth outlook ahead of elections.

- Hungary (REPHUN): Spreads tightened approximately -12bp to -20bp following an opposition election victory.

- Poland: Traded largely sideways over the week.

🌍 Sub-Saharan Africa

- SSA Sovereigns: Benchmark bonds were firmer earlier in the week (+0.5 to +1pt); sentiment remained cautious into latter sessions. The broader backdrop remained sensitive to IMF conditionality and fiscal risks.

🌎 Latin America

- Venezuela / PDVSA: Bonds rallied +1pt to +1.25pt amid firmer oil prices and IMF-related developments.

- Peru: Underperformed over multiple sessions following political developments, including the emergence of a left-populist challenger in the presidential runoff; price action remained contained but weaker relative to regional peers.

Corporate Credit

🇪🇺 EMEA Corporates

- Air Baltic: Bonds rebounded approximately +4pts after Latvia’s parliament approved a €30m loan to the airline, resolving a political dispute that had threatened coalition stability.

- DTEK Oil & Gas (Ukraine): Bonds rose +2–3pts following an exchange offer announcement.

- Metinvest (Ukraine): Reported FY2025 results including $130m in 2H free cash flow; stated intention to repay upcoming maturities.

🌍 Africa Corporates

- OCP Morocco: Secondary curve underperformed (-50c to -75c) following hybrid issuance guidance at approximately 6.75–7.375% yields; selling was observed from both real money and hedge fund accounts, though new issues held broadly stable.

🌎 Latin America Corporates

- Braskem: Bonds were broadly stable to slightly higher (flat to +0.25pt) following reports that coupon payments on 2034 notes were made. Earlier in the week, the complex had rallied +3.25 to +4.25pts before encountering selling at higher levels.

- Raizen: Bonds closed approximately +0.25pt higher after reports that bondholders proposed a restructuring plan including a capital injection of approximately BRL 8bn.

Market Tone

Across the week, improved macro conditions — including easing geopolitical tensions and supportive commodity dynamics — were not fully reflected in ex-Asia EM credit performance. Markets exhibited high dispersion and headline sensitivity, with flows characterised by selling into strength and selective positioning rather than broad spread tightening.

www.gembridgecapital.com

DISCLAIMER

This document is strictly confidential and is being provided to you for informational purposes only. It does not constitute an offer to sell or a solicitation of an offer to buy any securities or financial instruments. The information contained herein has been obtained from sources believed to be reliable but is not guaranteed as to accuracy or completeness. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice.

AI Generation Notice: Portions of this content may have been generated or assisted by Artificial Intelligence (AI) technologies. Users should independently verify critical data points. Past performance is not indicative of future results.

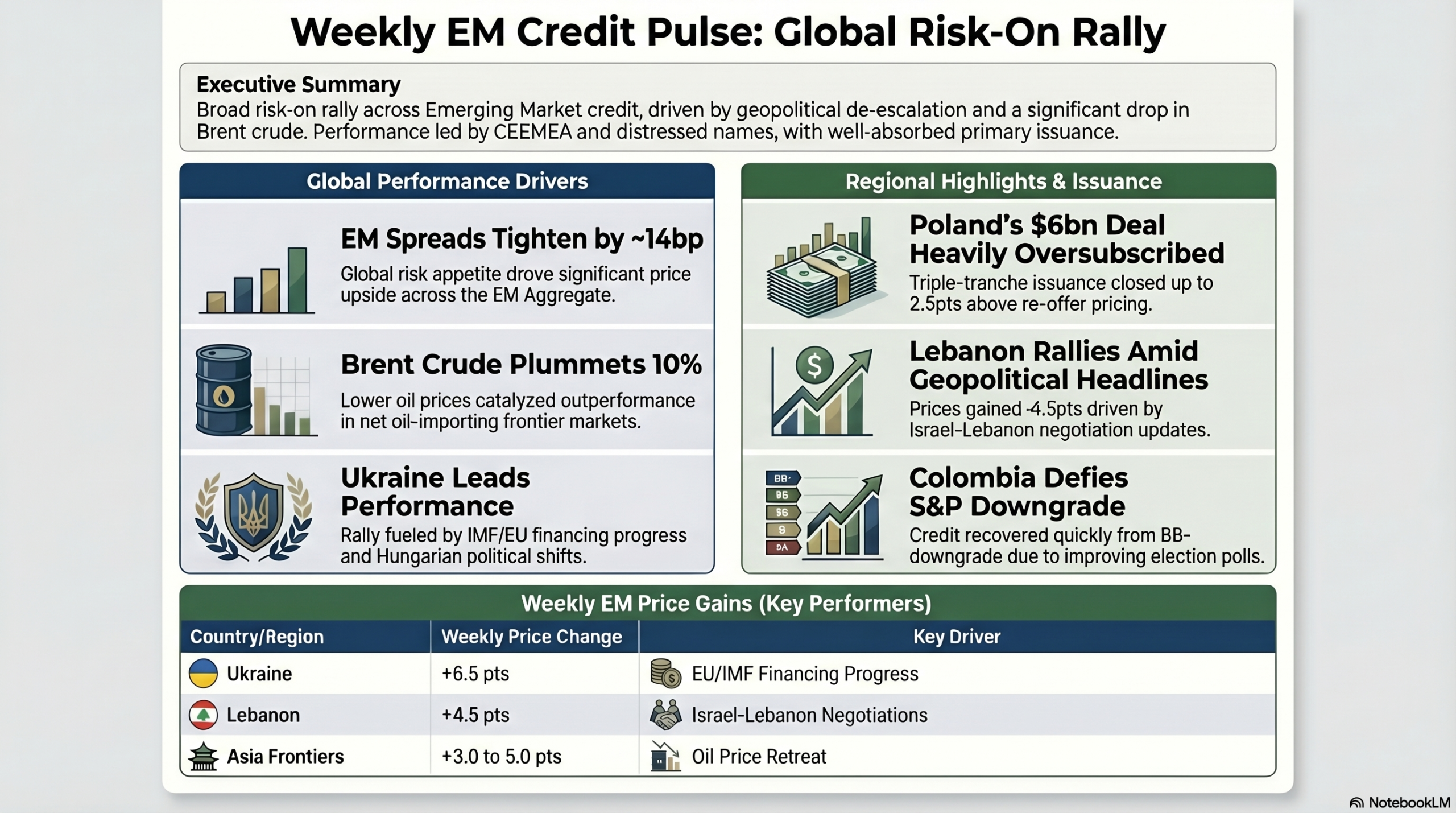

Executive Summary: EM credit spreads tightened broadly over the week. EM Aggregate spreads narrowed approximately 14bp w/w and CDX.EM gained close to 1pt. CEEMEA and distressed/high-beta names led performance; LatAm also finished the week firmer. In Asia, credit prices recovered sharply following a last-minute US–Iran ceasefire announcement, with Brent falling approximately 10% on the week. Asia IG returned +0.5% and Asia HY returned +0.9%. Asian equity markets rose between 3% and 11% across the region. Two-way flows were observed across HY and hybrid names.

Market Visualizer

Regional Credit Developments

🌍 EM Ex-Asia Credit

- LEBAN: The curve closed +4pt/+4.5pt w/w on turnover exceeding $550mm. Both hedge fund and real money accounts were active following Israel–Lebanon negotiation headlines. High PDI bonds closed approximately 1pt above the rest of the curve on the week.

- POLAND: Priced a $6bn triple-tranche deal (5y/10y/30y at T+65/T+105/T+130). New issues closed +1pt/+2.4pt above re-offer. The secondary curve closed -4bp/-14bp w/w.

- REPHUN: Activity increased ahead of Sunday’s elections. Polls from Median and 21 Kutatokozpont showed Tisza leading by 23% and 19% respectively among decided voters. The dollar curve closed -16bp/-28bp w/w; EUR bonds closed -12bp/-23bp w/w.

- UKRAIN: Best-performing EM ex-Asia credit this week — A +6.5pts, B +5.75pts, C +4.5pts w/w. Contributing developments included broader risk-on conditions following US–Iran ceasefire talks, reduced polling support for Orbán in Hungary ahead of Sunday’s election, and Ukraine’s parliament passing bills required for IMF and EU financing.

- DRCONG: Priced its inaugural dual-tranche dollar deal: $600mm 5y WAL at 8.75% and $650mm 10y WAL at 9.5%. Bonds traded as high as +1pt/+1.5pt above re-offer before retracing to close at approximately +63cts/+1pt above re-offer.

- COLOM: Bonds lagged Thursday morning following S&P’s overnight downgrade from BB to BB–. The curve recovered later in the week alongside broader market improvement. Polls indicated both Espriella and Valencia would outperform Cepeda in a potential run-off. The curve closed -18bp/-33bp w/w.

- VENZ / PDVSA: Headlines on Tuesday reported that the interim government and its political opposition were coordinating their legal defense of national assets. VENZ closed +85cts/+2pt w/w and PDVSA +1.75pts/+2.25pts w/w, near recent highs.

- Africa / SSA: Kenya and other net oil importers outperformed as Brent declined approximately 10% on the week. Moody’s completed its periodic review of Zambia with no rating change. Ghana’s outlook was revised to positive. SSA HY and distressed spreads tightened on the week.

🇨🇳 Asia Credit: China Property & HY

- Meituan: Fitch revised the company’s credit outlook to negative from stable.

- eHi: 63.51% of its due-2026 bonds were tendered for exchange, below the 85% minimum acceptance threshold. The company waived the minimum condition and the exchange proceeded.

- Medcij: Tapped its 2030 bond for $200mm at $103.072.

🌏 Asia Credit: Frontier & Sovereign

- Pakistan / Sri Lanka: Both closed up 3–5pts on the week. Adsez 41 and RWLVCAs each gained approximately 3pts on the week.

- Sri Lanka: The IMF and Sri Lanka authorities reached a staff-level agreement following the Extended Fund Facility (EFF) review. Access to approximately $700mm is contingent on completion of the Executive Board review.

- Sammaan Capital: Bonds closed approximately +1pt on the week. The company launched a tender offer for its 2030s at par, up to $45mm. Crisil upgraded its local rating to AA+.

- Philippines: S&P revised the BBB+ outlook to stable from positive.

www.gembridgecapital.com

DISCLAIMER

This document is strictly confidential and is being provided to you for informational purposes only. It does not constitute an offer to sell or a solicitation of an offer to buy any securities or financial instruments. The information contained herein has been obtained from sources believed to be reliable but is not guaranteed as to accuracy or completeness. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice.

AI Generation Notice: Portions of this content may have been generated or assisted by Artificial Intelligence (AI) technologies. Users should independently verify critical data points. Past performance is not indicative of future results.

Executive Summary: EM credit markets endured a volatile week as the Middle East conflict remained unresolved, dampening risk appetite across asset classes. Ex-Asia EM saw a sharp mid-week rally on US-Iran de-escalation hopes before fading as ceasefire credibility eroded. CDX.EM closed modestly firmer on the week, though ETF and real-money outflows from hard-currency funds persisted. In Asia, IG credit slipped 0.2% and HY fell 0.6%, with equity markets also under pressure (HSI -1.3%, KOSPI -5.9%). Vanke dominated headlines as it approached onshore bondholders for a payment delay and signalled potential broader restructuring. Selective bright spots emerged: IHFLIN bonds recovered on a Moody’s upgrade to B1, Zhongsheng rose post less-than-feared FY25 results, and Chinese tech names surged on the regulator’s move to end food-delivery price wars. Pakistan bonds weakened intra-week; over the weekend, the IMF announced a staff-level agreement for a US$1.2bn loan package, subject to Executive Board approval.

Market Visualizer

Regional Credit Developments

🌍 EM Ex-Asia Credit

- CEEMEA – GCC IG: Largely retraced to pre-conflict levels, underpinned by local buyer support, as early-week optimism around US-Iran de-escalation sparked material tightening in Bahrain, Egypt, and Jordan before sentiment reversed on fading ceasefire credibility.

- Turkey / South Africa: Both cheapened into week-end against a backdrop of rate volatility and FX concerns, standing out as underperformers within CEEMEA.

- Angola: The US$2.5bn Eurobond dominated SSA flow, initially trading firm on new-issue demand before drifting below re-offer as broader HY risk sentiment softened late in the week.

- Egypt: Tapped its 2033s amid active sovereign issuance, with the name benefiting from the mid-week rally before retracing. SSA economies broadly grappled with oil-shock spillovers from the unresolved Middle East conflict.

- Latin America – Mexico / Colombia: Spreads generally widened, with both names underperforming on ETF selling pressure and oil-linked fiscal concerns. Selective secondary activity was observed in Chile and Peru, which cheapened back toward recent wides.

- EM Hard Currency Funds: ETF and real-money outflows persisted across the week. CDX.EM closed modestly higher week-on-week despite two weak late-week sessions, reflecting the broadly mixed tone.

🇨🇳 Asia Credit: China Property & HY

- Vanke: Bonds fell approximately 4pts to the high 30s as the developer formally reached out to onshore bondholders requesting a payment delay on its April maturity, while simultaneously weighing options for a broader debt restructuring. The situation remains fluid with no resolution announced as of week-end.

- Weschi: Bonds dropped ~4pts following weak quarterly earnings, compounded by a Fitch outlook revision to Negative on its B rating. The agency cited uncertainty over free cash flow improvement, elevated overseas capital expenditure, execution risks in the ramp-up of offshore cash generation, and the potential application of a lower country ceiling.

- Zhongsheng: Despite an S&P downgrade to BBB- from BBB, bonds rose approximately 2pts following FY25 results that came in ahead of market expectations. Management noted liquidity remains adequate.

🌏 Asia Credit: Frontier & Sovereign

- Pakistan: Long-end bonds slipped approximately 1pt during the week. Over the weekend, the IMF announced a staff-level agreement for a US$1.2bn loan package, subject to Executive Board approval.

- IHFLIN (IHS Holding): Bonds rose approximately 0.3pts on net, with the intra-week surge of 3-4pts driven by RBI approval of the IHS equity investment (SEBI approval still pending) and a Moody’s upgrade to B1 from B2 with a Positive Outlook. Bonds gave back a portion of their gains as the broader market weakened into the close.

📊 Equity & Sector Observations

- China Tech – Meituan / JD.com: China’s market regulator moved to end the price war in the food delivery sector, providing a direct boost to both names. Meituan surged 8.5% and JD.com rose 4.7% on the week, standing out against broadly weak equity markets (HSI -1.3%, KOSPI -5.9%).

- EV / Lithium / Green Energy: The sector outperformed against the broadly weak equity backdrop. Market participants noted the ongoing Middle East conflict drew attention to oil supply dependency; EV and lithium-related equities rose on the week alongside commentary around the green energy sector.

www.gembridgecapital.com

DISCLAIMER

This document is strictly confidential and is being provided to you for informational purposes only. It does not constitute an offer to sell or a solicitation of an offer to buy any securities or financial instruments. The information contained herein has been obtained from sources believed to be reliable but is not guaranteed as to accuracy or completeness. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice.

AI Generation Notice: Portions of this content may have been generated or assisted by Artificial Intelligence (AI) technologies. Users should independently verify critical data points. Past performance is not indicative of future results.

Summary: EM ex-Asia credit remained under pressure for the week ending 13 March 2026. The dominant market theme was the divergence between oil-importing and oil-exporting sovereigns, as elevated crude prices — sustained by the ongoing Iran conflict — produced sharply asymmetric outcomes across the complex. Oil exporters outperformed broadly, while importers faced additional balance-of-payments stress. Idiosyncratic drivers — including a presidential primary in Colombia, an IMF programme request from Gabon, and a corporate restructuring filing — generated significant single-name activity alongside the macro backdrop.

🌐 Macro Theme: Oil Importers vs. Exporters

- Bifurcation: Elevated oil prices — driven by sustained geopolitical risk from the Iran conflict — produced a clear divide in EM credit performance. Oil-exporting sovereigns outperformed on the week; oil-importing sovereigns remained under pressure.

- Oil Importers Under Pressure: Egypt, Lebanon, and Turkey — all net energy importers — traded with a heavy tone. Real money selling was the dominant flow dynamic across the group, consistent with terms-of-trade deterioration concerns.

- Oil Exporters Outperformed: Venezuela/PDVSA and small EM oil-producing sovereigns rallied on the week, supported by real money demand and a broadly constructive energy backdrop. Gabon, a smaller oil producer, was additionally supported by an IMF programme catalyst (see below).

- Sector Read-Across: The oil price environment also weighed on HY airline credits — which face direct fuel-cost pressure — and contributed to a cautious tone in Dubai real estate bonds, both of which declined on the week.

🗺️ MENA

- Egypt — Underperformed: Egypt was among the weaker performers on the week. Flows were characterised by real money selling earlier in the week, with hedge fund and local demand on the other side. A mid-week technical bounce driven by hedge fund buying in the long end proved short-lived, and the curve leaked lower into the close. The long end underperformed the front end on the week. In CDS, hedge fund activity was broadly net positive on the 5-year tenor.

- Lebanon — Political Headline, Curve Lower: On Monday, Parliament voted through a two-year delay to elections — a development largely expected by the market. Initial flows skewed toward hedge fund selling before real money and hedge fund buyers emerged at lower levels. The curve closed the week lower overall.

- Dubai Real Estate — Heavy: Dubai RE bonds traded with a heavy tone on the week, declining alongside the broader cautious sentiment across the region.

🌍 Sub-Saharan Africa

- Gabon — Best Performer in SSA HY: Gabon was the standout name in the region, rallying on reports that the country formally requested an IMF programme. Healthy real money two-way flow underpinned Wednesday’s move, though profit-taking emerged later in the week. Gabon closed as the top performer in Sub-Saharan African high yield on the week.

🏛️ CEEMEA

- Turkey — Weaker; Basis Richened: The Turkish complex traded with a heavier tone, with real money and ETF selling the dominant flow, partially offset by sustained local demand. Notably, the CDS/cash basis richened on the week — 5-year CDS widened more than the equivalent move in cash bonds — a divergence that warrants monitoring.

🌎 Latin America

- Venezuela / PDVSA — Outperformed LATAM HY: Venezuela and PDVSA outperformed within the LATAM HY sovereign universe. Real money was a net buyer across the curve, while hedge funds and locals reduced exposure. Real money swap activity was also observed across the curve.

- Colombia — Rallied on Primary Election: Colombia was a positive outlier following Sunday’s presidential primary elections. The market responded constructively to the result, with the belly of the curve outperforming. Early-week flows were dominated by real money and hedge fund demand, met by local selling, before some profit-taking emerged toward the close. 5-year CDS tightened on the week.

- Chile — Mixed Flows, Broadly Flat: Activity picked up on Thursday with mixed flow dynamics — hedge fund basis selling, real money two-way, local demand, and ETF selling all observed. The net result was a broadly flat week for Chile cash. No major directional catalyst was present.

- Argentina — Quiet Week: Warrants closed broadly unchanged. The broader cash curve was modestly lower. No significant catalysts drove directional flow; the name traded in a holding pattern.

- Raizbz — Out-of-Court Restructuring Filed: Raizbz generated significant single-name activity after the company filed for an out-of-court restructuring arrangement. Post-headline demand from real money and hedge funds pushed bonds higher initially; however, real money selling re-emerged across the belly and long end toward week-end. The 27s underperformed the rest of the curve. The curve closed materially higher overall, though the near-term outcome of the restructuring process remains the key variable.

✈️ Sector Themes

- HY Airlines — Continued Weakness: Pressure on high-yield airline credits continued through the week. Bonds declined, consistent with the elevated fuel cost environment.

- Small EM Oil Producers — Rallied: Smaller oil-producing sovereigns rallied on the week, reflecting the direct pass-through of higher crude prices to sovereign credit metrics. This cohort was among the clearest beneficiaries of the oil price environment.

📡 This commentary is compiled from internal trading desk notes and is intended for informational purposes only.

It does not constitute investment advice or a solicitation to buy or sell any security.

Information may be incomplete. Use with caution.

Gembridge Capital · Singapore · Week Ending 13 March 2026